Inflation takes a nibble

A cost of living crisis has emerged as inflation bites hard into the things we really can’t avoid buying, for example energy and food where price rises have been eye-watering. In the latest figures for January, whilst falling for three months in a row, inflation remains painfully high at 10.1%[1]. Its impact is being felt widely across society, and the quality of our golden years is one area that seems to be suffering.

According to pensions trade body, The Pensions and Lifetime Savings Association (PLSA), for those wanting to enjoy a very basic standard of living in retirement, costs are 18%[2] higher than they were a year ago.

Price rises are putting pressure on our retirements in two fundamental ways. For those saving for retirement, they will need a bigger pot, meaning needing to squirrel away more each month or saving for longer. For those in retirement, they will need to increase withdrawals, meaning facing the prospect of running out and having to rely on the state pension for the remainder of their days.

We can see this pressure in surveys. According to AJ Bell, an online brokerage, upon retiring 1-in-10 will now work part time as a result of the economic gloom, and a further 1-in-10 will retire later than originally planned[3].

As such, for those thinking about retirement saving, it’s blurring an already opaque financial goal: the size of the pot we need to build for the lifestyle we want to live. Fortunately, the PLSA has attempted to provide some clarity by defining three different potential standards of retirement living.

Seeking the golden years we dream of

Research shows that just over three-quarters of us, 77%[4], don’t know how much we need in retirement. As with any loosely defined goal in life, it causes us to focus on the present at the expense of the future.

As such, The Pension and Lifetime Savings Association (PLSA), a trade body representing £1.3 trillion in UK pension schemes, have painted a picture to help us plan for retirement – detailing three different standards of living with a breakdown of the costs involved, including rises year-on-year on account of inflation. Of course, personal financial circumstances vary wildly and these must be taken as a rough guide.

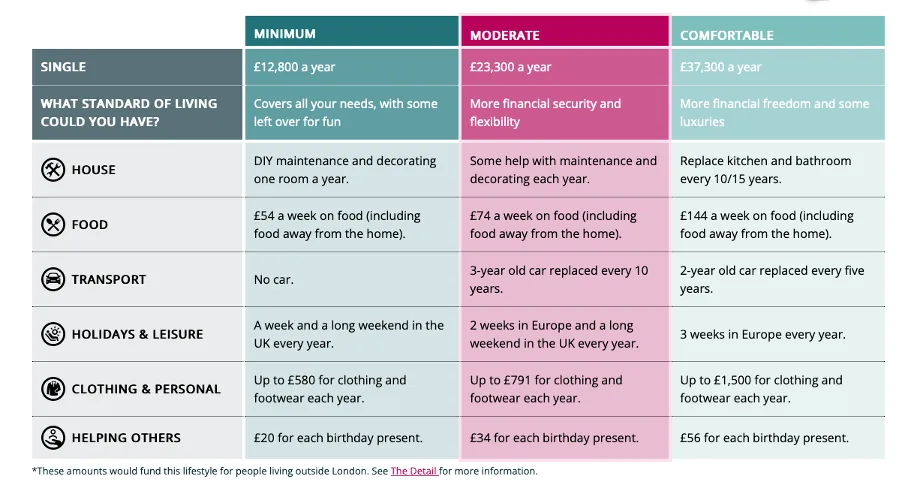

For a single person, the PLSA forecasts that you will need £12,800 a year to enjoy a ‘minimum’ standard of living in retirement (up 18% from last year), £23,300 a year for a ‘moderate’ standard of living (up 12%), and £37,300 a year for a ‘comfortable’ standard of living (up 11%). Below offers a picture of some of the things these standards will afford. Bear in mind these figures are different for a couple – please go to the PLSA’s Retirement Living Standards website for more details.

Source: Pension and Lifetime Savings Association

Meeting the standards

So, how do we go about paying for these annual costs? As a base, there is the state pension. If you have 35 qualifying years on your National Insurance record, you are entitled to the full state pension, which for the tax year 23/24 is £10,600 per year. For those with between 10 and 35 qualifying years, you will receive some degree of this.

This leaves it to us to make up the rest with our own private pot. Online investment brokerage AJ Bell has run some numbers to help us imagine the extra required. For those wanting a minimum standard, you’ll need a pot of £52,000[5], for a moderate standard it’s £354,0005, and for a comfortable standard, you’ll need a fairly hefty three quarters of a million, at £755,0005.

It means to be comfortable the savings goal is a fairly significant stretch. To put this in context, for those earning the UK’s average salary of £33,000 [6] and auto-enrolled into a company pension scheme contributing the minimum 8% of their salary, they would be unlikely to afford even a moderate lifestyle. As such, we need to make sure we’re making the most out of our pension savings.

Below are some tips for boosting your pension pot.

Our five top tips for making the most out of your pension

- Start as soon as possible – a long runway of growth and compounding does wonders for the size of your pot. It gives us an incentive to comb through our bills, cut anything we don’t need, and divert as much as we can to our pensions so that it’s not wasted.

- Use workplace pension schemes to add employer contributions to your own, which is a minimum of 3% by law. Some employers may be even more generous, or potentially match any additional voluntary contributions (AVCs) you may make.

- Boost your pot with any extras you might receive, for example bonuses or inheritance. Remember, you can contribute a maximum of £40,000 a year to your pension, or 100% of your salary, whichever is lower, and you may carry forward any unused allowance from up to the three previous tax years.

- Use private pension tax wrappers such as self-invested personal pensions (SIPPs) if you’re self-employed or wanting to contribute outside of your workplace pension. These come with tax relief and breaks to boost your pension savings.

- Get the most out of your state pension and fill in any gaps in your National Insurance record, which you may do so from up to the past six years.

[1] https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/consumerpriceinflation/january2023

[2] https://www.retirementlivingstandards.org.uk

[3] Source: AJ Bell, as of 05/01/23

[4] https://www.retirementlivingstandards.org.uk/details

[5] AJ Bell, as of 11/01/23

[6] Office of National Statistics, as of 01/10/22