By Faith Archer, personal finance journalist

Don’t worry if you are late to the starting a pension party, as you can still boost your retirement savings.

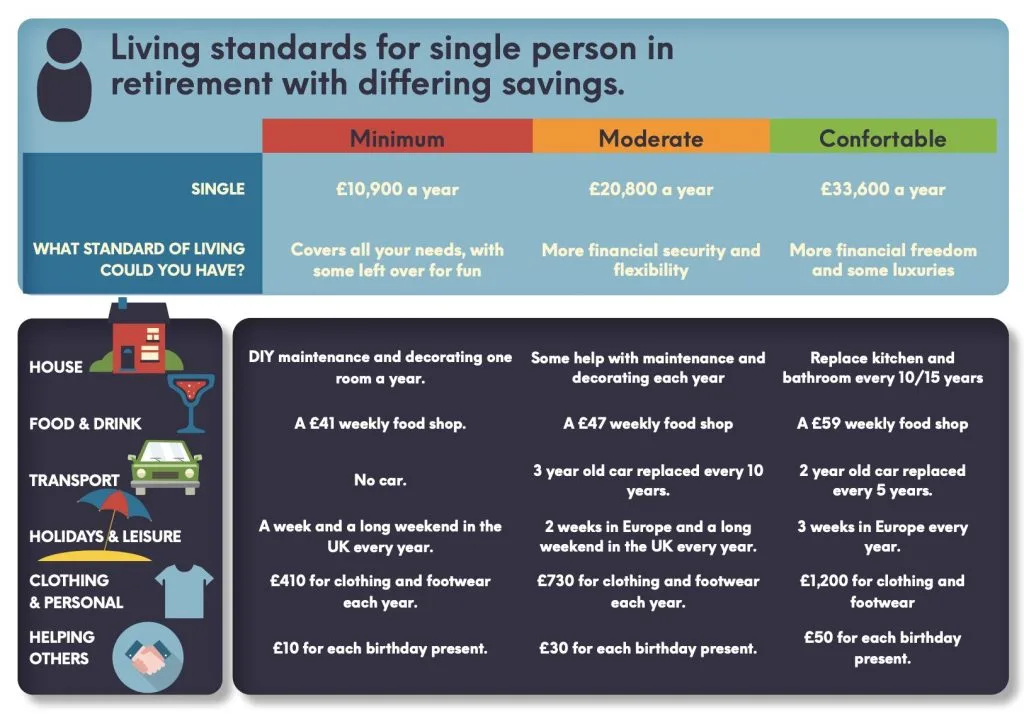

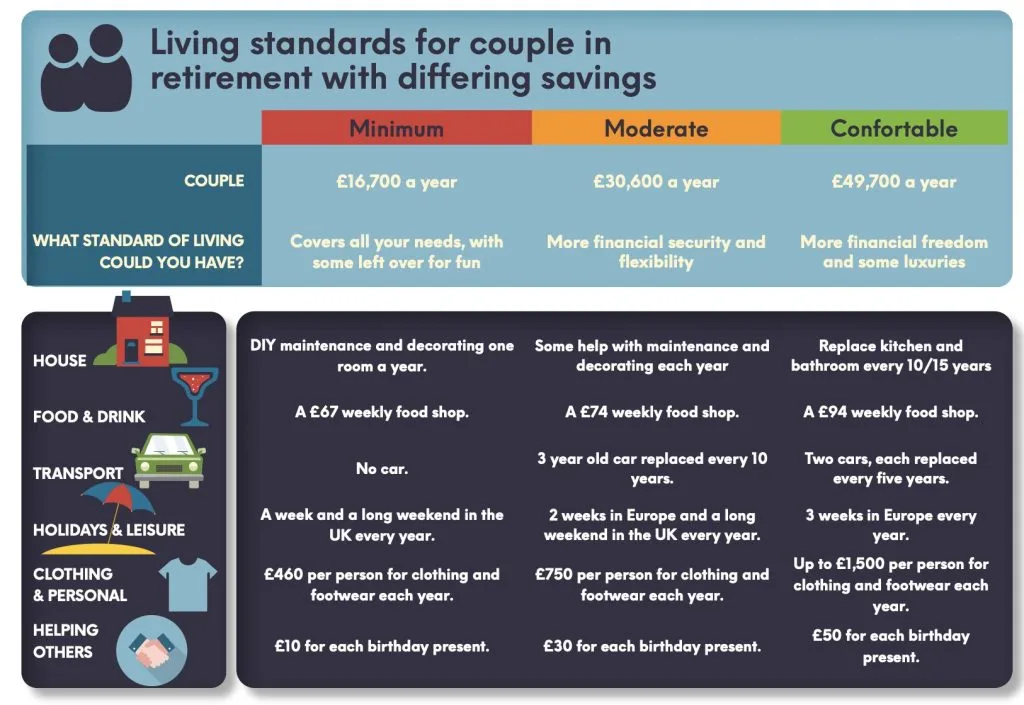

Sure, ideal world, we would all have started ploughing money into pensions way back in our twenties, with more time to contribute and more time for those contributions to grow. For a comfortable retirement, a couple needs £49,700 a year, or a single person needs £33,600, according to the Pensions & Lifetime Savings Association.

If your current pension won’t stretch that far, remember that even closer to retirement, you can still benefit from the free money added in tax relief. For every £1 you pay into a pension, you should automatically get another 25p added in basic rate tax relief. Higher and additional rate taxpayers can then claim back even more.

Fundamentally, to boost your pension pot you need to either pay more in or squeeze more out of your existing savings. Read on for tips and tricks to transform a smaller pension into something to celebrate.

1) Plough more into your pension

Typically, our peak earning years are during our fifties, so it may be easier to afford larger pension payments than when younger.

Go through your household bills and living costs, to see where you can make savings, then channel the money into your pension. Every time you get a pay rise, bump up your contributions, before you get used to living on the extra.

2) Divert previous payments

Shed any regular bills? Consider diverting those payments into your pension, for example if you clear your mortgage, pay off a car loan or finish contributing towards your children’s university costs.

3) Profit from work pensions

If you are a member of a pension at work, check if your employer is willing to pay in more than the 3% required by law. Some employers, for example, will match additional contributions by staff up to a certain point, so by upping your own payments you can nab more money on top.

It’s also worth checking if your employer will make a larger contribution to your pension if you switch to salary sacrifice. With salary sacrifice, you agree to give up part of your salary in exchange for a benefit such as higher pension payments, and you and your employer then pay less National Insurance on the reduced salary.

4) Large it with lump sums

Turbo charge your pension pot with lump sum contributions, for example if you receive a bonus or an inheritance. If you have spare cash earning next to nothing in a savings account, you might want to divert it into your pension and snap up the tax relief.

Most people can pay up to 100% of earnings, maximum £40,000 a year, into a pension and still rake in tax relief on top.

You can also ‘carry forward’ unused pension allowance from up to three previous tax years, if you would like to pay in a particularly chunky sum. However, you can’t pay in more than you’ve earned in the current tax year, and you must have been a member of a pension scheme during the previous years.

Higher earners also face restrictions on how much they can pay into pensions, while still receiving tax relief. Once your earnings top £240,000 a year, adjusted to include pension contributions, the tax man claws back £1 of pension allowance for every £2 of ‘adjusted income’ above this, down to a minimum pension allowance of £4,000 a year.

5) Conquer your cashflow demons

The self-employed can be reluctant to lock money away in pensions, concerned it might be needed earlier for investment opportunities or cash flow crises.

However, the tax relief can look increasingly attractive as you get closer to the age when you can whip money out, currently 55 but rising to 57 from 2028.

In later life you can therefore whack in larger sums, knowing you don’t have long to wait before you could access the money.

The first 25% of your pension pot can be withdrawn tax-free, but anything above that is taxed as income. Just bear in mind that if you do take out more than the 25% tax free, it will restrict how much you can pay into a pension in future, down from £40,000 a year to just £4,000.

6) Track down lost pensions

It can be all too easy to lose track of old pensions, if, for example, you move house and don’t let the pension company know your new address. Tracking down lost pensions can therefore help boost your retirement pot. Contact the pension provider (if you know who it is), speak to past employers or use the government’s free Pension Tracing Service online or on 0800 731 0193.

7) Cut your costs

Squeeze more out of your retirement savings by checking the fees charged for hosting your pension and for funds used. Transferring to a plan with lower charges means you hang on to more of your own money and it has more chance to grow. Just check you won’t be giving up valuable guarantees or benefits by moving your pension cash.

8) Review your investment choices

Check where your pension money is invested, and whether it matches your goals and attitudes to risk.

Watch out because as you move closer to retirement age, many pension plans automatically move your money out of shares in companies and into less risky options.

However, depending on how you want to access your pension, you might be better off hanging onto some stock market investments, with greater potential for growth.

If you opt for income drawdown, for example, your money may remain invested for a good 30 years or so. There is always a risk that prices can fall as well as rise, but that allows plenty of time to ride out stock market storms.

9) Top up your state pension

Lastly, don’t forget your state pension.

You can discover how much you should get at gov.uk/check-state-pension. If you have gaps in your National Insurance contributions, see if you can boost your state pension payments by making voluntary contributions – although normally you can only go back up to six years.

You can also boost payments if you take them later than normal state pension age. For every nine weeks you defer, you will get an increase of 1%, which adds up to 5.8% for every full year.

After deferring your state pension for a year, you would need to live for another 15 years to be quids in, according to calculations by AJ Bell. This assumes that the state pension increases by 2.5% a year, the current minimum increase.