Whether you’re thinking about sacking-off work to go travelling, buying your first home, or finally getting around to sorting a pension for retirement, we take you through all the essentials to start getting investing in your 20s and 30s.

In this guide, we run through:

- Why you need to be investing…right now!

- An important checklist before starting

- How stock markets work

- Building some financial goals and a plan: going travelling, first home, or retirement

- How to find the right platform & account

- Choosing the right investments for your goals

1) Why should I invest my money rather than save it?

The all important question. The key thing to remember with finance is that, if you want rewarding with some form a return, you must take risks. ‘Investing’ encompasses risk taking in financial markets in an attempt to try and receive a reward – that’s the other thing to remember, rewards are not guaranteed. Saving on other hand is virtually risk-free, so we don’t tend to get paid much for cash held in bank accounts.

Right now there has never been a more crucial time to invest. Inflation is the highest it’s been since the early 80s(!), yet bank interest rates remain at rock bottom. As a result, your cash will be receiving a NEGATIVE rate of interest, meaning tomorrow it will be worth less than it is today. Investing offers you the opportunity to beat the cost of living crisis through assets with returns that have the potential to stay ahead of inflation.

What is more, it doesn’t need to be the wild west of cryptos and single shares (but it can be if you like) – using funds is a great to invest without taking massive risks. And there’s lots of other techniques to reduce risks too that basically involve spreading investments around which is very effective. More on that later. Click to watch our animation on investing versus saving.

2) What do I need to sort before diving into the stock markets?

Let’s run through a few tips before you getting going with investing:

- Clear expensive debt – investment returns will NOT consistently beat the costs of credit cards or payday loans! Zero those first before investing – and for the love of…please don’t use them as a means to invest.

- Create a rainy-day fund – You need an emergency stash of readily available cash – the advice is 3-6 months of your living costs. Why? It makes funds available and massively reduces anxiety in the case of an emergency: if you need to fix a broken boiler or you face redundancy. Knowing you’ve cash on hand means you’ll sleep snoozy sleeps, even in the knowledge investments are running around in the stock markets.

- Insurance – a financial adviser will always talk to you about insurance, namely income protection in the case you lose a job, and life insurance if you lose…well, you get the picture. If you’re seeking extra comfort when investing, plenty of financial comparison sites will help you. We like MoneySavingExpert.

3) How do stock markets work?

Stock markets are where financial instruments (assets) associated with companies and governments are traded. Rather usefully, these instruments can be grouped together into assets classes: by far the largest are company shares, which represent a piece of ownership of a company, and are also known as stocks or equities; and bonds too, which represent loans made to companies or governments. But there’s plenty more: property, commodities, currencies, infrastructure, and others too.

What’s useful is that different assets classes come with different risks when investing. It means by choosing to invest in different assets, we can adjust how much risk we want to take, depending on our time horizons and how much risk we’re comfortable in taking. Very broadly, stocks are seen as much riskier than bonds, meaning the returns you receive can be much higher than bonds, but so can the loses. This is often referred to as volatility: the greater the volatility, the wider the potential swings in the price of an asset.

That said, there is a multitude of ways of reducing these risks, by spreading our investments around using funds and across markets and asset classes. It’s why investing doesn’t need to be scary: there’s a horse for every course. If you’d like to watch a quick 3-minute animations on these concepts, watch investment risk.

4) What should I consider when forming financial goals?

Financial goals represent the major financial milestones we wish to achieve in our lives. For those in their twenties and thirties, the most common are: going on that big holiday or career break, buying your first house, or starting a retirement fund. In order to know what mix of stuff to invest in, there are a couple of things to consider.

- First, the length of time you have to invest before you reach your goals. The longer you have, the riskier the assets you can invest in because you have time to allow market swings to recover from temper tantrums (which are very normal across longer market cycles).

- Shorter term goals – less than three years – travelling or big holiday

- Medium term – 3-5 years – buying your first house

- Longer term – 5-10+ years – retirement

- Second, your personal feelings towards risk – your risk appetite. Some investors can be more cautious than others, meaning the thought of assets sitting at a loss – even if just on paper – can make them uncomfortable. This requires some reflection, but may change as investors learn more and experience investing. This is a quick questionnaire to give you an idea of your personal risk attitudes. Top journalist Faith Archer has also written on our blog about her experience investing in the stock market for the first time.

Why is this important? Because it determines the types of asset classes you might want to invest in. As a very rough guide, you might want to consider these minimum timeframes for each asset class:

- <3 years – cash savings

- 3-5 years – bonds

- 5 years – shares, property

- 5-10 years – Alternatives, commodities

6) How do I find an investing service and open an account?

It’s important to find the right investing services for your approach and account for your goals. Fortunately, we’ve built lots of reviews pages to help you out. There are two bits to this process:

a) Finding an investing service:

- Keeping it simple – ‘do-it-with-me’ platforms, also called robo-advisors or digital wealth managers, are a slick new breed of investing service that usually offer a trim selection of very broad, cheap portfolios to invest in. Our DIWM platforms page explains what they do in more detail, and reviews the UK’s ten leading platforms.

- Getting stuck in – ‘do-it-yourself’ platforms are more traditional online investing platforms like Hargreaves Lansdown, interactive investor, and AJ Bell, offering a wide selection of investments and accounts. Our DIY platforms page explains more, with another review for the UK’s top ten DIY platforms.

b) Opening an account:

Once you have chosen a platform, you’ll need to open an account with them. There are two key accounts which have been designed by government and that come with generous tax perks:

- Stock & Shares Individual Savings Account (ISA) – for tax free investing, and there are four different types. We explain it all in our blog, everything you need to know about ISAs and we review the top ten ISA providers.

- Self Invested Personal Pension (SIPP) – for tax free investing with government top-ups but age restrictions. Read the full details on our SIPP page here and reviews of the top ten SIPP providers.

Back to our goals:

- Going travelling – both the DIY platforms and DIWM platforms have cash and low risk products for shorter term goals. Alternatively you could go to Moneyfacts to find out the best rates across UK cash products.

- Buying your first house – a nuance of the ISA: the Lifetime ISA is perfect for those wanting to save for a first house. You can invest up to £4,000 a year in them and the government will top you up with a 25% bonus, so potentially another £1,000.

- Building a pension pot – Open SIPPs at any of the major investment platforms, or you could even go for a more specialised service such as PensionBee, which is a simplified DIWM service focusing only on…yes, you guessed it…pensions!

7) Which investments are right for me?

a) Keeping it simple

The very easiest way to get going is by using one of the DIWM platforms. When you sign up, you will usually be asked to answer a few simple questions on your financial goals and attitudes to risk. Following this, you will be directed into one of a small collection of broad, multi-asset portfolios – between 7-10 is typical – each of which will differ in terms of investment risk: from low through to higher. Within each portfolio, there will be a number of cheap passive index trackers, investing your money widely across assets and markets around the world. As such, these services tend to be cheap, but won’t leave you with a lot to sink your teeth into. This approach is about starting it up, and letting it run!

b) A half-way house

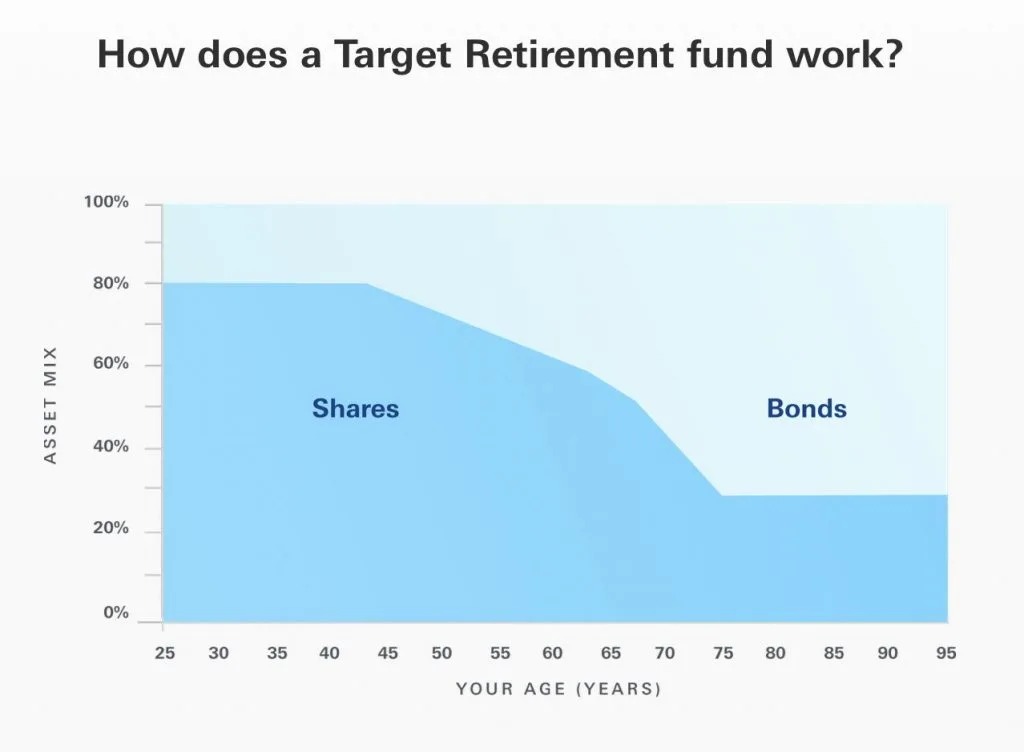

If you want to get a bit more involved, but still don’t want to think about asset allocation and investing in different markets, there’s a solution! You could open an account with one of the DIY platforms, and invest in either a multi-asset fund, or if you’re looking at retirement goals, a target date retirement fund.

A multi-asset fund is much like the DIWM portfolios, investing in a wide range of assets around the globe, the extend of which will depend on the fund’s objectives. A target date retirement fund will change the mix of assets in the portfolio and gradually reduce its risk the closer you get to retirement. Vanguard have a large range of these funds, and demonstrate the changing mix below.

c) Getting stuck in!

For those wanting to get fully involved – just open an account with a DIY platform and start thinking about the assets you want to invest in and adding diversification. One important decision is whether to choose a fund with a fund manager who makes investment decisions and attempts to produce index beating performance (never guaranteed though!), or you go for a passive fund which will simply replicate index performance, but for a much lower charge. Watch our video on funds and investment trusts.

Often we get asked on how best to review funds and choose the best ones. Fortunately, we have a blog on how to choose a fund written by Faith Archer.