Why is buying your first home so hard?

It’s a ladder that only seems to get steeper for the young in society: buying their first home. The problem is twofold. First, houses are already very expensive – in March, the average home cost £258,115[1]. And while the government has devised schemes to aid first time buyers, such as Help To Buy and Shared Ownership, the second problem is that broadly they’re becoming more expensive by the day. True, house prices have dropped over the past year as the double whammy of inflation and higher interest rates hits affordability, but this comes after many blistering years of double-digit annual growth. Given that pressures on the housing market are likely to ease over the course of the year as the heat comes out of inflation, prices are likely to resume their stomp in no time.

It means for first time buyers, by the time they reach their savings goal the goalposts are likely to have been moved. This means more saving and more time, and the tedious cycle is doomed to repeat. So, for those starting out with saving for their first home, how best to go about it? The answer lies with the Lifetime ISA.

How much do I need for my first home?

Circumstance largely dictates how much you need as location massively changes the cost of housing (see here for Nationwide’s House Price index for regional averages). But we can use averages. AJ Bell’s Laura Suter (hear her discuss investing for your children on the Steps to Investing Podcast) has run some figures. Over the past 40 years, the average annual price rise has been 5.5%. It means in ten years’ time, the average home will cost £417,913. Of course, there may be brief declines in the housing market, such as we’re seeing at the moment, but this feels like a good rough goal. Given that there are plenty of lenders offering 95% mortgages (they are more expensive though – check rates here at Moneyfacts), it means a minimum goal of £20,895.65 if you opt for a 5% deposit.

How do I save enough for my first house deposit?

One of the smartest ways to build your deposit is to invest your money using a Lifetime ISA. This is a subset of the general ISA, and works in a similar way. You put in money and the taxman can’t touch any interest, investment gains or income. The difference with the LISA is that it comes with a maximum allowance each tax year of £4,000 (which counts towards your £20,000 overall ISA allowance) but the really great feature is that the government – very generously – boosts any contributions with a 25% bonus. It means you could receive up to £1,000 in free cash every year. This will make an enormous difference to saving for a deposit.

How much do I need to save for a deposit?

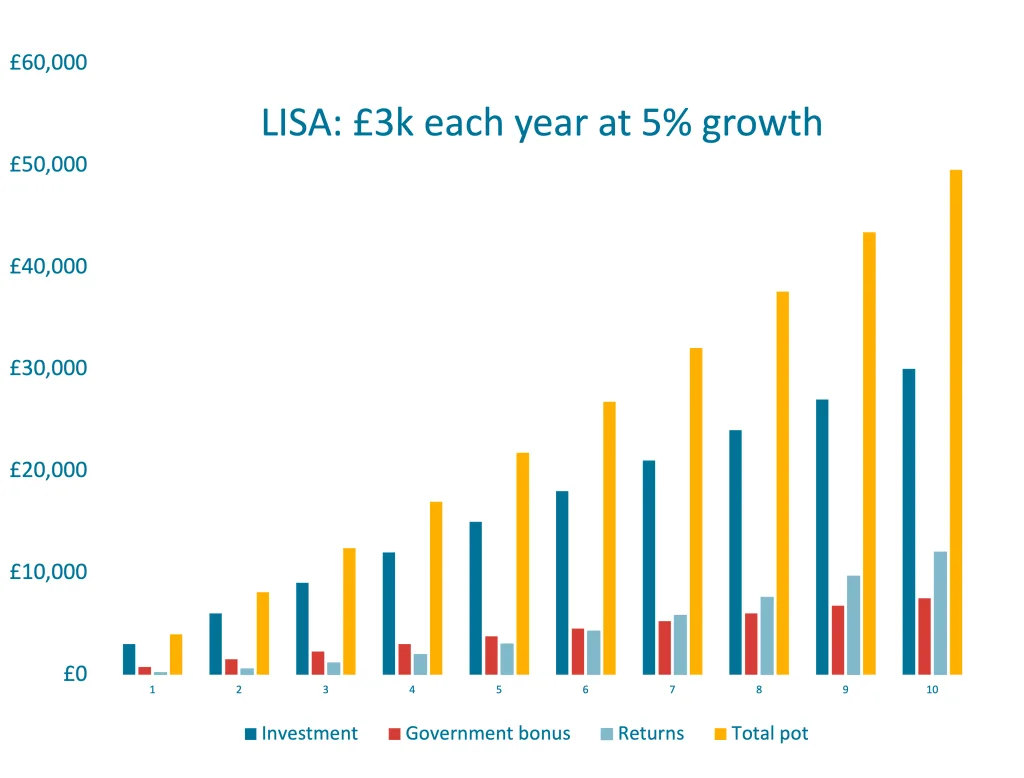

Stashing away £250 a month could leave you with a tidy pot. It equates to £3,000 per year, to which the government would add £750 in free money. Let’s assume you do this with the aim of buying a house in ten years’ time. With returns of 5% each year, this would land you with a deposit pot of £49,525, or 12% of our estimated future average house price. It seems more than enough.

The chart below shows the journey, and splits out your contributions, the free government bonus, the investment gains alone (you can see the power of compounding working here), and the total pot.

Are there other restrictions with LISAs?

There are some restrictions you must consider with LISAs. The money can only be used for one of two things: buying your first home, or after you’re 60 years old. Fairly obviously, the idea is only to assist with either getting on the housing ladder or retirement. The other restriction is that you have to be aged between 18-39 to open one – although you can continue to contribute into it up to the day before your 50th birthday.

[1] Nationwide House Price Index; March 2023