I remember receiving an annual bank statement through the post one day, and staring at the interest I was earning on about 10k of cash stashed away for travelling, thinking – WHAT?! The bank doesn’t value me much – I hate banks!

My account was giving me 0.4%. You might find likewise on your savings, and if you’re similarly frustrated/perplexed/infuriated, the next natural question is ‘what sort of returns can I expect in the stock markets’?

Investing in the hope of a better return – but how much better?!

First rule about investing: there are no certainties with returns, just (hopefully intelligent) assumptions that form a case about how an investor thinks an investment will perform. I could look at the future of the car industry and say electric cars seem like a good bet due to their greener footprint and belting performance round a track, and Elon Musk seems a pretty smart guy when he’s not insulting people over Twitter, so I’ll buy Tesla over, say, Ford. This is your investment case. But Tesla’s could uncover a technical fault that requires a global re-call of all its cars, which could cost lots of money and dent the cash it was expected to take over the year, hobbling the share price and the value of my investment.

These are the types of risks you take when investing in financial assets: the future can bring all sorts of unforeseen scenarios which may affect the value of your investments, which is why you won’t hear investors talking much about what you’re going to get back. And this makes sense: if returns were guaranteed, wouldn’t everyone already be doing it??

But rather than stop as this rather annoyingly vague answer, we could look to the historical returns of stock markets to offer at least some idea as to how might expect them to continuing performing.

Enter some smart chaps from Cambridge’s Judge business school and London Business School: Elroy Dimson, Paul Marsh, and Mike Staunton. They’ve compiled the returns of stock markets all the way back to 1900! The report is public – although perhaps a little dry for bedtime reading.

Investment returns over time – three perspectives

Financial investments tend to be grouped according to their shared characteristics and the way they behave in the markets, and will offer a certain amount of reward for the risks taken. The higher the risk, the greater the chance of reward, but also the greater the chance of loss. That said, it’s important to know that over the long term – as in, at least a decade – markets tend to go up, and so should your investments.

Here, we look at three different groupings to give you an idea of how the risks and potential rewards can differ. Ultimately, by understanding and being able to identify these different groups, will you know roughly what returns to expect from investing in them. We will go into more detail in all of these areas further along the Steps.

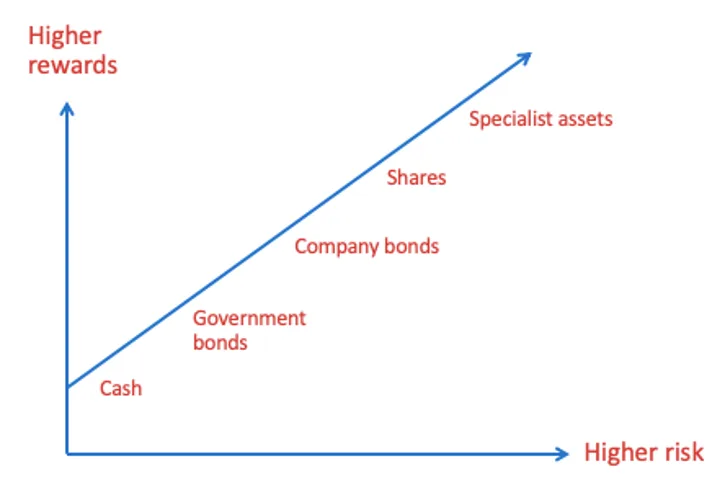

1. Returns from different asset classes

Asset classes represent the very top level grouping, see our video here. Below is a rough graph to give you a broad idea of the risks and rewards that are expected for basic asset classes:

To explain why this is the case, let’s use companies as an example. Businesses fund themselves either through taking on debt, by taking out loans or issuing bonds, or through selling shares in the company, also known as its equity.

There are numerous reasons why shareholders face greater risks when compared to bondholders: ultimately they face much less certainty of payment as they are far less of a legal priority in a corporate’s financial structure, and so tend to be more richly rewarded.

Here are the UK’s yearly returns of the two over 120 years:

UK shares vs bonds: +5.5% vs. 1.9%

It shows that £100 invested in UK shares in 1900 would have given you back £61,701, whereas bonds would’ve given you £957.

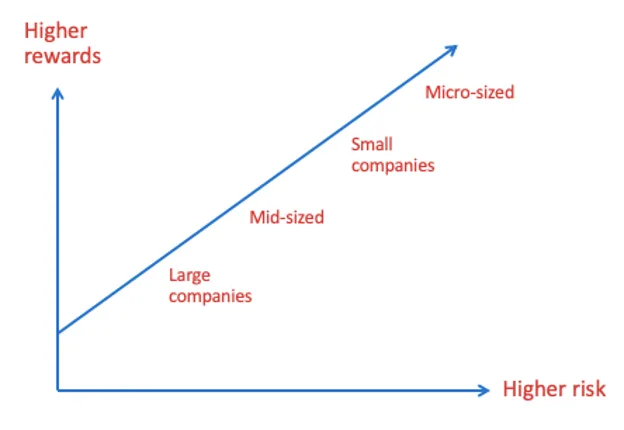

2. Returns from different size companies

As you can see in the chart, the size of a company will determine the returns you get form its bonds or equities. Just think – is your local Chinese takeaway more or less likely to go under than Coca-Cola? Now think of the reasons why: lower profitability, dependence on narrow markets, reliance on a particular business owner, and so on.

Because smaller businesses tend to have smaller product ranges with less diverse operations and cash to fall back on, their share prices generally suffer greater extremes, so the market will give you a greater reward over the long term.

Here’s the yearly shareholder returns from different size businesses in the UK since 1955:

- Micro: + 17.4% (valued less than £150m)

- Small: + 15% (valued between £150m – £500m)

- Mid-sized: +13.7% (valued between £500m – £4bn)

- Large: + 11.7% (valued more than £4bn)

This means £100 invested in large UK stocks in 1955 would have returned you £7,261 today, whereas micro stocks would’ve landed you £3.38m!

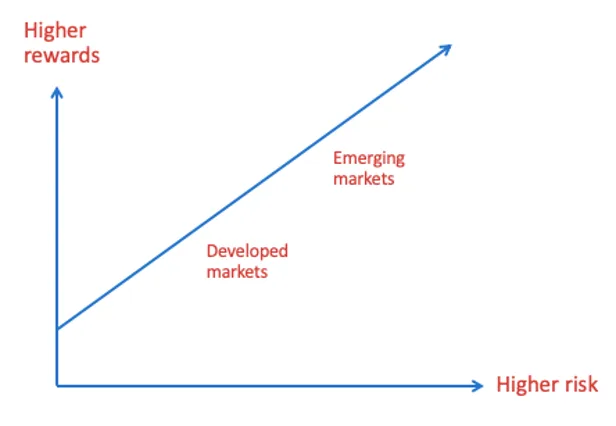

3. Returns from different markets?

So, what did the data say about the yearly returns from different markets over 120 years:

- US shares +6.5%

- European shares +4.3%

- Japanese shares +4.2%

Different markets will have differing levels of financial sophistication, political stability, sound economics, and therefore performance. As a general rule: emerging markets like Brazil or China will have more risk but bigger rewards over the long term when compared to developed markets such as the US or UK.

Tips to Investing

- Take a long-term approach to investing.

- If you are young and have even longer, you can take more risk.

- Spread your investments across different asset classes and markets to avoid taking too much risk in any one area.

- Learn how to invest with Steps to Investing.