Given the UK’s FTSE-100 was one of the best performing stock market indices in 2022[1] – a particularly tough year for stocks – you would’ve thought it would curry more favour amongst investors. Apparently not.

According to funds network Calastone, whilst company shares were broadly shunned by UK fund investors throughout a dismal 2022, with £6.29bn in outflows averaged across all equity (share) sectors, the intensity of selling at UK-focused funds was individually worse, seeing £8.38bn in outflows – a dreary record. It’s not a picture that’s improved this year either: the selling has continued every month in 2023.

This seems perplexing. So, why has the UK stock market has become so unpopular with British investors?

A chilly climate

For more than a few years, the UK has been left standing out in the cold by investors. A host of factors are responsible. Most recently, the idiosyncrasies of Brexit, the pandemic, and Tory political turmoil have made UK shares non grata as the economy and government finances have gradually deteriorated.

If we broaden our scope and look at markets since the global financial crisis, we see investors have tended to prefer the ‘new economy’ technology and growth companies of the US stock market, and shun the ‘old economy’ banks, miners, energy, financials, and tobacco stocks that broadly adorn the Footsie.

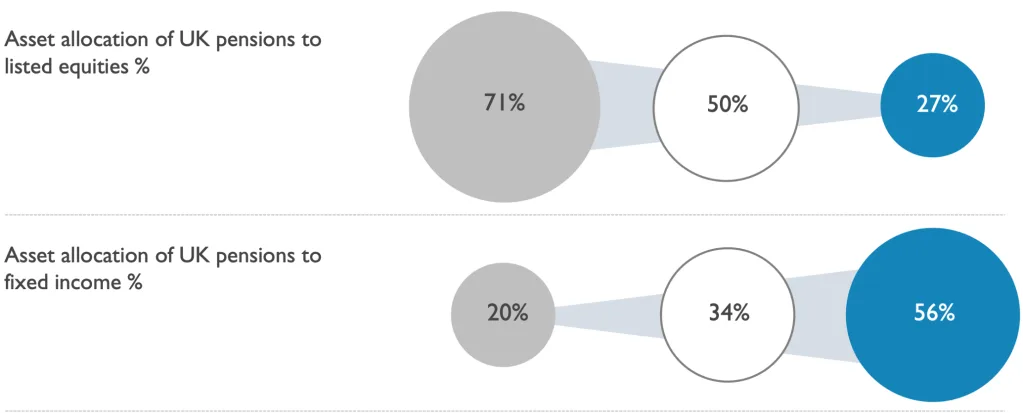

And yet, expand our time horizons again, and we find another powerful force looming over UK markets. Since the late 1990s, successive changes to regulation, tax and accounting standards here have led to a significant shift in risk appetite across UK pension funds and insurers, now managing a whopping £4.6 trillion in assets[2]. As such, not only have they wound down the portion of shares in their portfolios and significantly increased holdings in bonds (fixed income) to better match their long-term liabilities, but they’ve also sought a more exotic variety of overseas equities in their remaining allocation, kicking UK equities to the curb2.

We can see the dramatic shift in allocation below, years from left to right: 2000, 2010, 2020.

How the UK market has been affected

The impact has been to pressure UK markets through the continued selling of UK stocks, which weighs on prices; at the end of day, they are simply a result of the interplay between buyers and sellers in the market. As a result, the UK stock market has seen a long period of lacklustre returns in comparison to other markets, for example the US. As we look back over 25 years – which includes the disastrous dotcom crash – the US stock market has grown by nearly three times in value; the FTSE100, on the other hand, is just 31% higher[3].

It means – and back to our conundrum of why UK shares are not more popular following a stellar 2022 – investors seem to be simply cashing-out following a dire few decades in the UK’s stock market.

And yet, as the world economy changes gear for the first time in a while, there are reasons to believe that a sea change could be underway for the UK stocks, and that, finally, the FTSE might be the stock market to tip.

Changing fortunes

There’s a number of reasons to believe why investors may warm to UK stocks.

First, the ‘old economy’ cash-generative financials, miners, and energy stocks have become significantly more attractive in a world of higher inflation and rising interest rates. It’s why UK markets performed so well in 2022. These may continue to do well if elevated inflation and higher interest rates are here to stay, which is possible if trading across the global economy fragments amid higher geopolitical tensions and governments start increasing spending in areas such as green infrastructure and defence.

Second, the UK stock market continues to look cheap when compared to its own history[4] and other markets such as the US[5]. Whilst some may believe this is justified, investing when markets are cheap usually yields much better results over the long term than when they appear overpriced. Warren Buffett is one of the most famous proponent of this value-based approach.

Third, if things become more dire in the economy, for example if higher inflation and interest rates continue to ratchet-up the pain on UK consumers and businesses, then the low valuations of UK shares may act as a buffer against overly severe falls.

Fourth and finally, the UK market is a bone fide strong dividend payer. In a world where higher inflation persists, dividends serve as a great source of income, as companies, to varying degrees, have the ability to raise prices which should translate into higher profits and dividend rises that at least have a fighting chance of keeping-up with inflation.

[1] https://www.telegraph.co.uk/business/2022/12/30/london-beats-rivals-worlds-best-performing-major-stock-market/

[2] https://capitalmarketsindustrytaskforce.com/wp-content/uploads/2023/03/2023.03-Unlocking-the-capital-in-capital-markets-New-Financial.pdf

[3] https://www.google.com/finance/quote/.INX:INDEXSP?comparison=INDEXFTSE%3AUKX&window=MAX

[4] https://simplywall.st/markets/gb

[5] https://simplywall.st/markets/us